Pisceans are notorious for being dreamy and idealistic. But is a quasi-public trading platform for unlisted companies the solution UK capital markets really need, or an ill-fitting solution to a problem that needs more fundamental reform?

Against a backdrop of collapsing numbers of new issuances and growing rates of de-listing either through corporate take-overs or PE take-privates, the London Stock Exchange is pressing ahead with the creation of Pisces, a new intermittent trading venue (ITV). Chancellor Rachel Reeves will announce in her Mansion House speech tomorrow that the enabling legislation will be coming forward as early as May next year. The idea was originally conjured up by the last Conversative government and so must logically have run the Labour gauntlet of “not invented here”, yet somehow survived.

New entrant in an already well-developed UK market for private capital fundraising

Few would doubt that it makes sense to have an effective route map for companies which may ultimately end up on the public capital markets. But the case for a new route to liquidity remains unclear when set in the context not only of the current, highly developed market for institutional private equity but also the state of other junior markets currently on offer.

Every year, commentators point to the weight of dry powder still waiting to be deployed by institutional funds (both debt and equity) that is looking for a home in UK private businesses. For those companies looking to attract investment, an entire community of advisers aims to ensure that they are fully aware of their options and can be brought to market in a structured, efficient way that best matches risk capital with potential rewards. Investors themselves have long-since got in on the act too, running teams of in-house deal originators to scour individual sectors and sub-sectors to unearth investable propositions. Once they have completed their first tour of duty with private equity on board, investee companies can now look forward to a potentially limitless number of PE owners, thanks to multi-billion pound funds and highly liquid debt markets. And for devotees of the role of public companies in opening up investing opportunities to the retail investor, it’s not as though the UK is short of options at present.

Multiple alternatives for public capital have already been shown to have played out

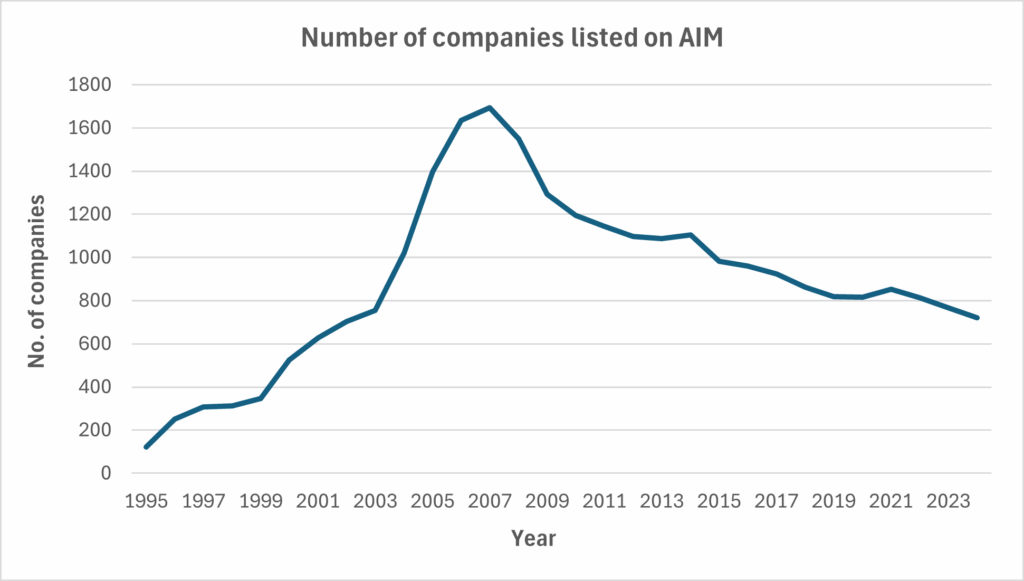

The Alternative Investment Market (AIM) was launched nearly 30 years ago as a replacement for the Unlisted Securities Market (USM) – itself something of a proto-ITV. Its principal strategic aims were (1) to help growing companies to raise growth capital, including for acquisitions, and (2) to smooth the transition to full listing, starting with a lighter regulatory burden. Following a steady start, AIM’s popularity exploded in the mid-2000s but the index has seen a near-constant decline in the number of companies listed on it since then. Its total market value may have grown but this belies the truth that for many AIM-listed companies, a lack of scale and liquidity have been continuously punished by investors who have simply ignored them.

Other pretenders to the throne have faired little better, with Aquis Exchange struggling to attract more than 100 companies in total. Barely one third of those have a market cap exceeding £10m and half of all companies in the index are worth less than £5m. This week’s announcement that the Aquis bourse itself is being acquired by the privately owned SIX Group is simply dripping with irony.

Was crowdfunding an equality of opportunity for retail investors, or just a casino for the uninitiated and unsuspecting?

In a post-GFC world, crowdfunding promised to democratise the process of raising early-stage capital which had, up to that point, been the preserve of business angels and institutional VCs. Platforms such as Seedrs and Crowdcube now provide private companies with a structured means of issuing new capital to investors and in many cases a secondary market in which to create liquidity for their unlisted shares. But the ultra-light touch regime and a focus on slick, five-minute pitching videos can arguably distract investors from even the most basic due diligence that they would apply to much larger, fully-listed share purchases. There appear to be precious few instances of crowdfunding investors sitting on cash following a successful exit and many for whom the next meaningful contact after investing is from an insolvency practitioner.

Is Pisces swimming against the tide of reality?

Private companies looking for funding will often complain about a lack of suitable options. Debt can be in short supply and private equity can be too expensive for all but the highest growth companies. Public companies will for their part bemoan the short-termism of stock market investors and a lack of understanding of their business’s real value. Prudent management of cash, if it results in a cut to dividends, will be punished even though the alternative would be reckless. And without adequate coverage by analysts or an effective market-maker, it can be almost impossible to provoke a timely and evidence-based re-assessment of smaller listed companies’ valuations.

An ITV, by its very design, offers only limited opportunities for investors to express their latest view on the value of a company. What chance is there for management to adequately communicate the investment thesis and to explain their strategy effectively? And because companies are not likely to be able to raise new equity through Pisces, there is a genuine risk that each trading window offers merely a “bear pit” for speculators looking to profit from the unsuspecting, less well-informed retail investor.

Creating the “big businesses” of tomorrow is already a well-practiced artform

One argument being thrust forward in support of Pisces is its possible role as a means of smoothing the transition to public company status. The Treasury claims that the new exchange will “support these businesses to grow”; as if access to money was the sole determinant of success. But on this issue too, it seems that the world has simply moved on already and that PE has developed a level of sophistication that the new platform simply cannot compete with.

For many years, PE-backed businesses have gone through a multi-year “boot camp” in which their internal systems, controls and processes are uprated prior to an ultimate exit. Whether this be to a corporate acquirer, another PE investor or an IPO, this process of internal maturity allows management teams and their businesses to prepare properly for the rigours of being a “big business” (or at least a part of one).

The wrong solution to a real-world problem

However well intentioned, it seems that the Treasury and the Stock Exchange are woefully behind the times with this latest proposal. We should applaud the desire for innovation and a potential “bonfire of the red tape” by government, at least in so far as it supports the growth of UK businesses.

But the shortage of IPOs and the trend of de-listings isn’t going to be solved by this proposal. To achieve that, we need a more fundamental review of the role of public markets in the economy. Like its astrological namesake, the plan for Pisces is living in a dream-like state from which the Treasury will soon have to wake up.

For more information or to discuss how we may be able to help you, please contact Kristian Gavan.